Can I Sell My Car If It's on Finance

Find out if you can still sell your car with outstanding finance, in our latest guide.

Discover how Hire Purchase works at Bristol Street Motors. Whether you're looking for new car deals or used car deals, we can help you find the ideal Hire Purchase finance plan for your needs.

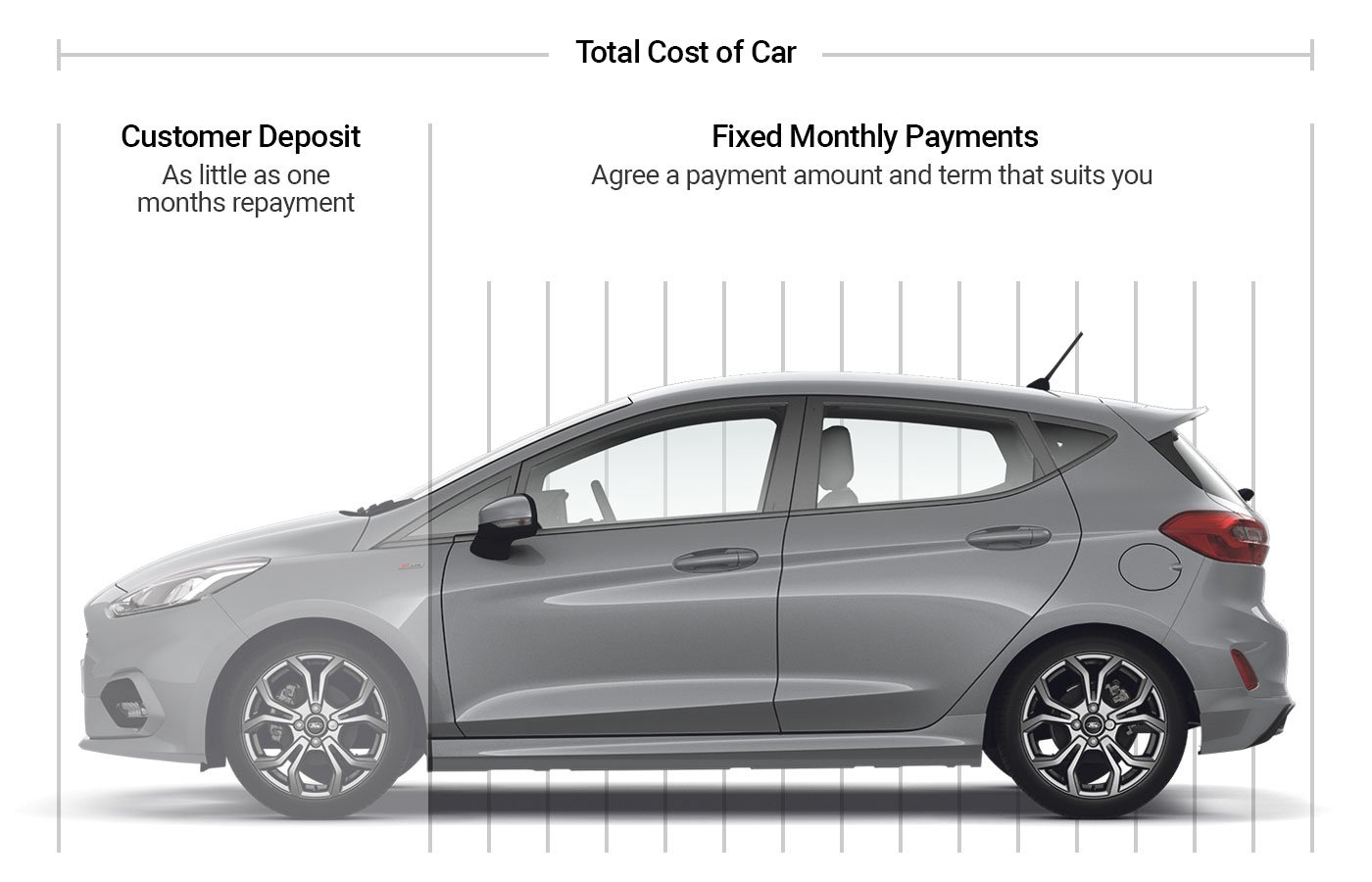

Hire Purchase is a popular finance option for new and used cars including electric vehicles. You will pay an upfront deposit followed by fixed monthly instalments for the duration of the agreement.

At the end of your contract, you will own the vehicle outright, providing you have made all the monthly payments and a small Option to Purchase fee.

Your deposit will typically be around 10% of the vehicle's value, and contracts usually last between 12 - 60 months. However, these terms can be flexibly negotiated when you set up your Hire Purchase plan.

Explore our wide range of new and used cars. Whether you prefer to browse online or at your local dealership, our friendly team are on hand to offer their expert advice.

Once you have weighed up your finance options and decided that Hire Purchase is the finance plan for you, we can get started.

Use our finance calculator to build your personalised Hire Purchase contract. You choose the deposit and length agreement that works for you.

When selecting your car finance, it's important to evaluate which plan works best for you. Here are the main advantages of Hire Purchase:

If you're considering a Hire Purchase contract, there are a few things to note.

Firstly, you need to be over 18 years old to apply for any type of car finance.

Additionally, your credit history will be assessed when you apply for Hire Purchase finance. The lender will conduct checks, to evaluate whether you can manage the repayments.

Getting a personal loan may be difficult if you have a poor credit rating. However, with a car finance plan such as Hire Purchase, the finance is secured against the vehicle. This basically means that if you are unable to keep up with the repayments, the lender can repossess the car. This could make Hire Purchase a more accessible option than a loan in the case of poor credit.

If you pass the finance company's credit check, the lender will generally approve your application for finance.

Representative Finance Example For Online Purchases |

|||||

|---|---|---|---|---|---|

| Customer deposit | £99 | ||||

| Monthly payments | £272.01 | ||||

| Cash Price | £15,000 | ||||

| Amount of credit | £14,901 | ||||

| Fees | £0.00 | ||||

| Optional final payment | £6,912 | ||||

| Total amount payable | £20,067.48 | ||||

| Annual mileage | 8000* | ||||

| Term | 48 months | ||||

| Fixed rate of interest | 6.15% | ||||

| Representative APR (fixed) | 11.70% | ||||

| Customer deposit | £2,158| Monthly payments |

£227.90 |

Cash Price |

£10,956 |

|

| Amount of credit | £8,798 | ||||

| Fees | £0.00 | ||||

| Total amount payable | £13,097.20 | ||||

| Term | 48 months | ||||

| Fixed rate of interest | 6.09% | ||||

| Representative APR (fixed) | 11.70% | ||||

What is a balloon payment on Hire Purchase?

Hire Purchase agreements do not have a balloon payment like Personal Contract Purchase agreements do. However, 'balloon payments' in relation to Hire Purchase deals may refer to the Option to Purchase fee. This is the final amount you need to pay to own the vehicle at the end of the contract. The Option to Purchase fee in a Hire Purchase plan is much less than a balloon payment on a personal contract purchase.

Can you pay off Hire Purchase early?

Yes. According to Section 99 of the Consumer Credit Act 1974, you have the right to voluntarily terminate a Hire Purchase contract. However, you must have paid at least half of the finance amount.

You will need to request a valid settlement letter which will detail how much you have left to pay in order to exit the Hire Purchase agreement.

If you haven't already paid off half of the finance amount, you can pay a lump sum to bridge the difference.

You may also have to pay a termination fee, so it's worth bearing this in mind.

If you would like more advice on this topic, get in touch with our friendly team.

Can you modify a car on HP finance?

You will only be able to modify the vehicle once you have paid it off in full, at the end of your Hire Purchase contract. While the agreement is running you are not the legal owner of the car, so you shouldn't make any modifications to it.

Once you own the car outright, you can make the modifications you would like.

Can you sell a car on Hire Purchase?

With Hire Purchase, you aren't the legal owner of the car until you have made all the payments and paid the Option to Purchase fee. The lender remains the owner of the vehicle up until this point. Therefore, you must wait until you are the legal owner to sell your car.

What is a Hire Purchase agreement?

Hire Purchase is a type of car finance for new and used cars. It involves paying an initial deposit alongside fixed monthly payments for an agreed length of time. At the end of the term, you can pay an Option to Purchase fee to own the vehicle outright.

Hire Purchase is a great finance option if you want to pay for your car in manageable monthly costs that are fixed. It is also ideal if you know you want to own the vehicle at the end of the agreement.

At Bristol Street Motors, we offer a wide range of Hire Purchase deals across our new and used car range. Contact us to see how we can help you find your next car at a great price.

What's the difference between Hire Purchase and personal contract purchase?

With a Hire Purchase contract, you effectively pay monthly to 'hire the vehicle. You only ever own the car once you have made all the payments and have paid the Option to Purchase fee. Hire Purchase is an ideal option if you want to own the car at the end of the agreement.

With personal contract purchase (PCP), you pay monthly towards the predicted depreciation costs of the car. When the agreement comes to an end, you have three options:

The most common option is to exchange the car for a new one, taking out a new agreement. PCP may be a more suitable finance option if you would like to drive a new car every few years.

What's the difference between Hire Purchase and personal contract hire?

With Hire Purchase, you pay a deposit and monthly instalments to effectively 'hire' the car until you own it. Once you have made all the payments and paid an Option to Purchase fee, you will own the vehicle.

With personal contract hire, you pay monthly to effectively 'lease' the vehicle, but you must return the car at the end of the agreement. This finance type is ideal if you want to drive a new car but know you don't want to own it at the end of the contract.

Personal Contract Purchase (PCP) is a popular finance solution for new and used cars. It involves an initial deposit, fixed monthly payments, and flexible end-of-term options.

Learn more about PCP

Personal Contract Hire (PCH) is a common finance option, mostly used on new cars. You'll pay an initial rental followed by fixed monthly payments. At the end of the contract, you return the vehicle.

Learn more about PCH

Find out if you can still sell your car with outstanding finance, in our latest guide.

In this guide, we will cover everything you need to know about HP and PCP finance so you'll have a better understanding when you come to buy your next car.

Find out what the laws are around cancelling car finance plans should you need to before the agreement end date.

We are a credit broker and not a lender. Finance is subject to status and finance company acceptance. We can introduce you to a limited number of lenders and their finance products. We will typically receive a commission from the lender, as either a fixed fee or a fixed percentage on the amount you borrow. The commission we earn does not change by the type of finance. A guarantee may be required. The finance rate will vary dependent of customer personal circumstances for in dealership purchases.